First-Time Car Buyer: Your Guide to Buy Your First Car

Buying your first car is a major milestone. Whether you plan to buy a new car or a reliable used car, understanding financing, dealership tactics, and maintenance will help you make informed choices. This first-time car buyer guide covers everything you need to know before you hit the lot so you can feel confident about the car purchase and the monthly car payment you’ll accept.

1. How do I decide between a new car and a used car when shopping?

Choosing new or used comes down to budget, expected depreciation, and the car you want. A new vehicle often carries higher price of the car and faster initial depreciation in the first five years, while a used vehicle can provide better value and lower monthly car payments. Consider whether the peace of mind of factory warranty and new model features outweighs the savings that come with buying used.

Think about total cost: the car purchase price, insurance, maintenance, and the car loan interest rate. If you have better credit you may qualify for lower financing rates on either new and used cars, especially from a bank or credit union. For first-time buyers, a certified pre-owned option can be a middle ground: newer, inspected used cars with a warranty that reduce uncertainty about the car’s condition.

2. What should a first-time car buyer know about financing and car loan options?

Financing is central to your car-buying process. Compare offers from dealerships, banks, and credit unions to find the best car loan rate. Credit score and credit history heavily influence your car loan rate: a higher credit score often yields better financing terms and lower monthly car loan payment. Getting pre-approved gives you negotiating power at the dealership and allows you to know exactly what you can afford.

When calculating monthly payment, factor the loan term, interest rate, and whether you plan a larger down payment. A longer loan reduces the monthly car payment but can increase total interest paid and risks owing more than the car. Consider a balance between comfortable monthly car payments and a realistic timeline to pay off the car without straining your budget.

3. How do dealerships set prices and what should I expect when I go to a dealership?

Dealerships price cars based on market demand, vehicle condition, and inventory needs. New car pricing often includes incentives, rebates, and destination fees, while used car dealers price based on the car’s history and local demand. When you go to the dealership, know the value of the car you want and the price of comparable vehicles so you can negotiate confidently.

Expect upsells at the dealership like extended warranties, add-ons, and gap insurance. Separate the vehicle price from financing and trade-in discussions—this keeps you focused on the price of the car itself. If you’re buying from a dealer, ask for a breakdown of fees and consider checking the car’s value on trusted sites to verify the dealer’s asking price.

4. How does my credit score affect my ability to buy a new car or used car?

Your credit score determines what financing offers you get. Better credit typically secures lower interest rates and more favorable loan payment terms. First-time buyers with limited credit history may benefit from building their credit through a credit union, using a co-signer, or taking out a small secured loan before applying for a larger auto loan.

Review your credit report before shopping so you know your credit history and can dispute any errors. Improving your credit or choosing a shorter loan term can reduce the amount you pay in interest, but may increase the monthly car payment. Balance short-term affordability against long-term cost to find the right financing approach.

5. What are the advantages of getting pre-approved for financing before I buy my car?

Getting pre-approved from a bank or credit union gives you clarity on the loan payment you can manage and makes you a stronger car buyer at the dealership. Pre-approval simplifies the buying process, helps you stick to a budget, and prevents dealerships from steering you into higher-rate financing. It also helps you compare dealership financing offers effectively.

Pre-approval reveals your likely interest rate, the maximum loan amount, and the monthly car payment estimate. Armed with this information, you can negotiate the car’s price rather than the monthly figure alone. Consider this an essential step for first-time car buyers who want to proceed with confidence and avoid unexpected issues when completing the paperwork.

6. What should I look for when buying used: inspections, history, and value?

When buying used, obtain a vehicle history report, look for service records, and have a trusted mechanic inspect the car. Check for title issues, prior accidents, and whether the car was regularly maintained. A thorough inspection can uncover problems that affect the car’s safety, the value of the car, and future maintenance costs.

Compare the asking price to market values to determine if the dealer’s price is fair. Consider common issues for the make and model, expected repair costs in the first few years, and total cost of ownership. Reliable cars often cost more upfront but save money on repairs and keep monthly costs predictable for first-time buyers.

7. How much should I plan to put down and how does a larger down payment help?

A larger down payment reduces your loan amount, lowers your monthly payment, and decreases the risk of becoming upside down (owing more than the car). Aim for at least 10–20% down if possible; more than that will reduce interest paid over the life of the loan. For first-time car buyers, a larger down payment makes financing easier and can improve your loan terms.

Putting more down can protect you from immediate depreciation that often occurs when you buy new. It also reduces the chance you’ll need to roll negative equity into a future car purchase. Work out different scenarios to see how down payment size affects monthly car payment and overall cost so you can choose an affordable option.

8. Should I trade in my current car or sell the car privately?

Trade-ins simplify the buying process because the dealership handles the paperwork and applies the value toward your new purchase. However, used car dealers may offer less than a private sale. Selling the car privately can yield a higher price, improving your down payment and lowering your loan amount.

Weigh convenience against price. If you need to buy your car quickly, a trade-in at the dealership can make sense. If maximizing the value of your current car is important, prepare it for sale, set a competitive price, and be ready to negotiate. Either way, know the trade-in value beforehand to avoid accepting low offers.

9. How do I estimate ongoing costs like maintenance, insurance, and registration?

Calculate the total cost of ownership beyond the purchase price. Cars need to be maintained regularly, and the first five years can include scheduled maintenance, tire replacement, and occasional repairs. Insurance rates vary by car, age, and driving history—get quotes before buying. Registration and taxes also add to first car purchase costs.

Consider fuel economy, expected reliability, and parts availability when choosing a car. A slightly more expensive but reliable model may cost less to maintain and insure over time. For first-time buyers, building a maintenance fund and following the manufacturer’s recommended service schedule will help you keep the car in good condition.

10. What are practical car buyer tips for negotiating and finalizing the deal?

Start negotiations from the vehicle price, not the monthly car payment. Use research on invoice and market prices, and be ready to walk away if the terms aren’t right. Get any verbal promises in writing and review the contract for add-ons you didn’t agree to. Ask questions about warranties, return policies, and dealer fees before signing.

Inspect the car on delivery, confirm that promised repairs were completed, and ensure that documents like title and registration are correct. If financing through the dealership, compare the final offer to your pre-approval. These car buyer tips help first-time buyers navigate the buying process with confidence and avoid regret after taking the car home.

11. How will I know if I’m choosing the right car and enjoying my new or used vehicle?

Choosing the right car means matching the vehicle to your daily needs, budget, and longer-term goals. Test drive the car in real-world conditions, assess comfort, visibility, and whether the car can handle your commute and lifestyle. Think about the car you want versus what you actually need—this balance will help you enjoy your new vehicle without overpaying.

After purchase, maintain your car according to the schedule, keep records of service, and monitor any unusual sounds or warning lights. Whether you buy new or used, a proactive approach to maintenance keeps the car reliable and preserves its value if you decide to sell the car or trade it in for your next car.

12. What should first-time buyers do after they buy the car to protect their investment?

After you buy the car, register a car in your name, update insurance, and keep all purchase and financing documents in a safe place. Follow a regular maintenance plan and address recalls or service bulletins promptly. Keeping the car well-maintained protects its value and reduces long-term ownership costs.

Monitor your car loan payments and avoid missed payments to improve your credit history. If you plan to sell the car later, maintain service records and clean the car regularly to maximize resale value. These simple steps help first-time buyers protect their investment and enjoy a smoother car ownership experience.

13. How do I balance buying the car I want with financial responsibility?

Buying the car of your dreams is exciting, but financial responsibility means setting realistic boundaries. Establish a total budget for the car purchase, including taxes, fees, and ongoing costs. If the car you want pushes your finances too far, consider alternatives like a used version of the same model, a smaller loan, or delaying the purchase until you save a larger down payment.

Use tools like monthly car loan payment calculators to see how different loan terms and down payments affect your budget. Balancing desire and practicality will ensure your first car purchase is a positive experience, not a financial burden.

14. Where can I find good car deals and reliable used cars for sale?

Search across dealerships, online marketplaces, and local listings to compare car deals and used cars for sale. Certified pre-owned programs at dealerships often provide added confidence. Check reviews and ratings for used car dealers and verify service records and inspections before you buy.

If possible, work with reputable used car dealerships or independent dealerships with strong customer service. Local credit unions and banks can also offer competitive financing that, combined with a fair purchase price, results in a great overall deal for first-time buyers.

15. What final steps should a first-time car buyer take before taking the car home?

Before you take the car, confirm paperwork, insurance, and any financing terms. Inspect the car one more time, verify that agreed repairs or detailing are done, and get copies of all contracts. Understand the warranty coverage and service expectations for new and used cars.

Make sure the dealer registers the car if required, or get the registration forms you need. Arrange to make your first car payment on time and set up autopay if helpful. These final steps ensure a smooth transition from shopping for a car to owning one.

Conclusion

First-Time Car Buyer’s Guide: Everything You Need to Know Before You Hit the Lot sums up the key steps: research new and used options, check your credit score, get pre-approved, inspect used vehicles, negotiate price, and plan for ongoing costs. Follow these car buyer tips to make a confident, informed car purchase that matches your needs and budget.

When you’re ready to shop for reliable used cars for sale, consider trusted local options like Integrity Autoplex, a Used Car Dealership in Elkhart, IN. Integrity Autoplex is among reputable used car dealers that can help first-time buyers find the right car while offering transparent pricing and financing options. Whether you’re comparing dealerships or exploring certified pre-owned vehicles, use this guide to buy your car wisely and enjoy the buying experience.

Frequently Asked Questions

What should I check before buying my first car?

Verify vehicle history, inspection, test drive, financing options, insurance rates, and total out-the-door cost.

Should I buy new or used as a first-time buyer?

Used cars save money on depreciation; new cars offer warranties and lower maintenance—choose based on budget and risk tolerance.

How do I negotiate the best price?

Research market prices, get preapproved financing, be willing to walk away, and focus on out-the-door price rather than monthly payments.

Bad Credit Car Loans and Auto Financing in Elkhart: How to Secure a Car Loan

Securing an auto loan in Elkhart with less-than-perfect credit can feel overwhelming, but with the right strategy and knowledge of local financing options, you can find a used car that fits your needs and budget. Whether you’re exploring bad credit financing, rebuilding your credit, or comparing dealerships and credit unions in Elkhart, this guide walks you through practical steps to qualify for a car loan, improve your credit situation, and drive away in the right used vehicle.

How can I find the best financing and auto financing in Elkhart with bad credit?

Start by researching local car financing options, including used car dealerships, credit unions, and online lenders that specialize in bad credit car loans. Elkhart has a mix of dealerships and finance centers where finance teams work with buyers who have low credit scores or credit issues. Use search terms like “auto financing in Elkhart,” “bad credit financing,” and “used car loan” to find lenders that advertise flexible loan terms and payments to the credit bureaus to help with rebuilding your credit.

Compare loan terms, interest rates, monthly payment estimates, and whether the dealer reports payments to the credit bureaus. Consider both buy here pay here and traditional lenders—buy here pay here can help you secure a car quickly, but the loan terms and interest rates may be higher. A credit union or an auto group with a finance center may offer better rates if you qualify, so get pre-qualified or pre-approved via online credit application to know where you stand.

What are the best steps for car shopping and finding the used car I deserve in Elkhart?

When car shopping in Elkhart, list your priorities: budget, size, fuel economy, and must-have features. Use local car lots, online listings, and visit used car dealerships to find a vehicle that suits your needs. Ask about certified pre-owned options, vehicle history reports, and any dealer warranties to protect your purchase. Finding a car that matches your financial needs makes it easier to secure a loan that fits your monthly payment goals.

Create a short list of vehicles and compare estimated car loan monthly payments using online calculators. Talk to the finance team at multiple dealerships and ask for a breakdown of loan terms, down payment requirements, and whether they offer bad credit financing or special programs for rebuilding your credit. Being prepared helps you negotiate better and avoid stepping away from approved car financing that doesn’t fit your budget.

How can I improve my credit score or rebuild my credit before applying for a car loan?

Improving your credit score increases your chances of qualifying for better loan terms. Start by reviewing your credit histories from the credit bureaus, disputing any inaccuracies, and focusing on on-time payments. Make a plan to pay down high-interest debt and keep credit card balances low. Small, consistent steps like paying bills on time and reducing balances can make a measurable difference when you apply for a credit card loan.

Consider secured credit cards or small credit-builder loans from a credit union to demonstrate responsible credit use. Ask lenders if the finance team reports payments to the credit bureaus—this helps you rebuild your credit when you make timely car loan payments. Remember, improving your credit takes time, but demonstrating progress can still help you qualify for a used car loan even if your credit situation isn’t perfect.

Which financing options should I consider: dealerships, credit unions, or online lenders?

Each financing option has advantages. Dealerships and their finance centers often have access to multiple lenders and can arrange bad credit financing through subprime lenders. This convenience can be helpful if you need a quick auto loan in Elkhart. However, dealer-arranged loans sometimes come with higher rates, so compare offers carefully.

Credit unions typically offer lower interest rates and flexible terms if you can qualify. They are ideal for buyers looking for affordable car financing with better loan terms. Online lenders and auto groups also provide pre-approval and allow you to apply online, often giving transparent rates. Use an online credit application to compare offers and choose the car loan company to suit your car finance needs.

How does my credit situation affect the auto loan application and loan terms?

Your credit score and credit history heavily influence interest rates, required down payment, and the maximum loan term you can access. Lenders evaluate types of credit, payment history, recent delinquencies, and your overall debt-to-income ratio. A low credit score or past credit issues may lead to higher interest rates or require a larger down payment to secure approval for a used car loan.

Even with a low credit score, you can qualify for bad credit car loans if you demonstrate steady income and manageable monthly payment expectations. Be transparent about your credit situation when completing a credit application at the dealership or online. Some finance centers specialize in helping buyers with credit problems and can help you find a loan if your situation demands flexibility.

Can I apply online and get approved quickly for an auto loan in Elkhart?

Yes, many dealerships, credit unions, and online lenders offer an online credit application that speeds up the approval process. Applying online allows you to get pre-qualified or pre-approved, compare rates, and see estimated monthly payments before visiting a used car dealership. Quick Auto South Bend and neighboring markets like Goshen and Mishawaka also have online options that can help you shop across nearby car lots and dealerships.

When you apply online, gather the necessary documents: proof of income, proof of residence, ID, and details about your current credit obligations. This preparation reduces delays and increases your chances of being approved for an auto loan. Make sure to ask if the lender reports payments to the credit bureaus to aid in rebuilding your credit over time.

What documents and financial information will help me qualify for a car loan?

Prepare the following to strengthen your loan application: recent pay stubs or proof of income, bank statements, identification (driver’s license), proof of insurance, and proof of residence. If you have previous car loans or credit accounts, having a record of on-time payments can help show lenders you’re managing credit responsibly despite past problems.

If you have a co-signer or can provide a down payment, mention this during your loan application—both can improve approval odds and get you lower interest rates. Consider working with a credit union or finance team at a used car dealership that specializes in bad credit financing to ensure your documentation is complete and accurately submitted.

Should I consider a cosigner or a buy-here-pay-here dealership when my credit is poor?

A co-signer with good credit can greatly increase your chances of securing a used car loan and getting better loan terms. A co-signer shares responsibility for the loan, which reduces the lender’s risk and can lower your interest rate. Make sure both parties understand the obligation, as missed payments can affect both credit histories.

Buy here, pay here dealerships can be an option if traditional lenders decline you. They often finance in-house regardless of credit histories, but watch for higher interest rates and stricter repayment terms. If you choose buy here pay here, confirm whether payments are reported to the credit bureaus—this can help with improving your credit score if you make timely payments.

How can I compare loan offers and choose the best car loan company to suit my needs?

Use a checklist to compare offers: interest rate (APR), loan term length, monthly payment, down payment, fees, and whether payments are reported to the credit bureaus. Ask each finance team to provide a clear loan breakdown and use online calculators to confirm that monthly payments fit your budget. Don’t forget to compare offers from local auto groups, credit unions, and dealerships in Elkhart, South Bend, Mishawaka, and Goshen.

Negotiate where possible. If you have multiple approvals, leverage them to get better terms. Remember that the total cost of the loan matters more than the monthly payment alone—look at total interest paid over the life of the loan. Choose a lender that offers transparency and suits your long-term goal of improving your credit and maintaining reliable payments.

What should I do after getting approved to protect my credit and rebuild my credit?

Once approved and driving the car, make on-time payments a top priority. Set up automatic payments or reminders to avoid late payments that could further damage your credit score. Confirm the lender reports your payments to the credit bureaus, so consistent on-time payments will help build your credit over time.

Monitor your credit reports periodically to ensure accuracy and to watch for improvements. Continue working on improving your credit by reducing other debts and avoiding new credit openings unless necessary. Staying consistent with payments and communicating with your finance center if you face hardship can prevent repossession and help you rebuild your credit history for future car buying.

Can bad credit hold you back from the perfect car, or are there realistic paths to get the next car?

Bad credit can affect interest rates and choices, but it doesn’t have to hold you back from finding the perfect car. With the right approach—shopping at reputable used car dealerships, finding lenders who offer bad credit financing, and preparing a solid credit application—you can qualify for a car loan that meets your needs. Focus on realistic expectations, such as choosing a reliable used vehicle and agreeing to manageable loan terms.

Use resources around Elkhart and nearby cities to increase your options. Work with finance teams that help you rebuild your credit and seek lenders that tailor loan terms to your situation. If needed, start with a modest used car loan and use responsible payments to improve your credit, paving the way to better financing for your next car.

How do I avoid common mistakes when applying for bad-credit car loans?

Avoid these common mistakes: applying to too many lenders in a short period (which can lower your credit score), not reading loan terms carefully, and agreeing to add-ons that increase your monthly payment. Always verify the APR, total loan cost, and whether the dealer reports to the credit bureaus. Be wary of offers that sound too good to be true—some predatory lenders target buyers with poor credit.

Get everything in writing and take time to review the finance contract before signing. If possible, get pre-approved and compare that offer to what the dealership presents. This comparison helps you negotiate better and prevents you from stepping into a loan that doesn’t suit your financial goals. Use objective checklists and consult consumer resources to make informed decisions.

What local resources in Elkhart and nearby communities can help with used car financing and credit support?

Leverage local credit unions, community financial counseling services, and reputable used car dealerships around Elkhart, South Bend, Goshen, and Mishawaka. Credit unions often have programs to help members with low credit scores, and community organizations may offer free or low-cost credit counseling. Local auto groups and finance centers can also connect you with lenders that specialize in bad credit car loans.

Visit multiple car lots and dealerships to get a sense of available inventory and financing offers. Ask about any dealer incentives, certified pre-owned vehicles, or special bad credit financing programs. Use these local resources to build a plan that helps you secure a used car loan while improving your credit for future purchases.

Conclusion: Key takeaways to secure an auto loan in Elkhart with less-than-perfect credit

- Research local financing options: dealerships, credit unions, online lenders, and buy here, pay here dealers.

- Get pre-qualified or pre-approved with an online credit application to understand your loan options and estimated monthly payment.

- Improve your credit where possible: review credit reports, pay on time, and reduce balances to increase approval odds.

- Prepare documentation: proof of income, ID, bank statements, and proof of residence to speed up approval.

- Compare loan offers carefully: APR, loan term, total cost, and whether payments are reported to the credit bureaus.

- Consider a co-signer or a modest down payment to secure better loan terms and lower monthly payments.

- Choose a reputable used car dealership or finance center that helps you rebuild your credit and provides transparent loan terms.

- Make timely payments and monitor your credit to improve your credit score for your next car.

When you’re ready to find a car in Elkhart, Integrity Autoplex, a Used Car Dealer in Elkhart, IN, can help connect you with bad credit financing, used car financing, and trusted used car loans. Integrity Autoplex and other reputable used car dealerships work to help you secure a no-credit car or a car loan regardless of your credit history, offering options to help you rebuild your credit and get back on the road with confidence.

What to Expect When Shopping at a Used Car Dealership: Tips for Buying a Used Car

Shopping for a used car can be one of the smartest and most budget-friendly ways to buy a car, but knowing what to expect when shopping at a used car dealership is crucial. Whether you’re stepping into a used car dealership for the first time or you’ve bought pre-owned vehicles before, understanding financing, inspections, negotiation, and the buying process will help you get the best deal and find a used vehicle that suits your needs.

What financing options will a used car dealership offer?

When visiting a used car dealership, ask about financing options up front. Many used car dealerships offer in-house financing, partnerships with a bank or credit union, and third-party lender options. Dealerships often advertise competitive interest rates, but the actual interest you qualify for depends on your credit score, the car’s age and mileage, and the loan term. Comparing offers from your bank or credit union before visiting can help you negotiate a better deal and understand how much you can afford for your monthly payment.

Before you buy a used car, calculate the total cost of the car including taxes, fees, interest rates, and any add-on warranties. Financing can alter the cost of a car significantly, so consider both monthly payment and total cost. If a dealership offers financing, ask for a breakdown of fees and whether they roll costs like extended warranties into the loan. This helps you make an informed decision and know what to expect when shopping for used cars.

How do you inspect the car at a used car dealership?

Inspecting the car is one of the most important steps when shopping at a used car dealership. Start with a visual check: look for mismatched paint, rust, and uneven panel gaps which could indicate past damage. Check the mileage against the vehicle history report and ask the dealer for maintenance records. Dealerships often have certified pre-owned vehicles that include more rigorous inspections and reconditioning, but even then you should inspect the car yourself and request proof of any work done.

Always insist that a mechanic inspect the car before you finalize the purchase, especially if you’re buying a used vehicle that isn’t certified. A mechanic can spot issues that a buyer might miss during a test drive or a quick walk-around. Many buyers bring a trusted mechanic to the dealership or request an independent inspection; don’t hesitate to ask the dealer to accommodate this — it’s crucial when buying from a dealership and will help you know what to expect when shopping for a used car.

What should you look for on the vehicle history report?

A vehicle history report is essential when shopping for a used car at a dealership. The report will reveal the vehicle history including previous owners, accident history, title status, odometer readings, and service records. Used car dealerships should provide this report on request and many list it online with used cars for sale. Reviewing the vehicle history can help you avoid cars with salvage titles, flood damage, or rolled-back mileage.

Use the vehicle history information to negotiate the price or decide whether the make and model you’re considering is worth the risk. If the vehicle history report shows regular maintenance and no major accidents, that can be a good sign and may justify a higher asking price. If it reveals problems, ask the dealer for a lower price or walk away — understanding the vehicle history helps you get the best deal and protect your investment.

How should you approach a test drive at a used car dealership?

One of the top things to expect when shopping at a used car dealership is a thorough test drive. A test drive lets you evaluate how the car handles, brakes, accelerates, and feels overall. Test the car under different conditions: highway speeds, stop-and-go traffic, and in parking maneuvers. Listen for odd noises and pay attention to how the car shifts, as transmission issues can be expensive to fix.

Bring a checklist to the test drive and take your time — don’t let pressure from sales staff rush you through. If you can, test drive the car at the time of day when you’ll commonly drive it (for example, during rush hour if you commute). If the car doesn’t meet your expectations or you feel unsure after the test drive, ask to inspect another vehicle or take more time to weigh your options. A proper test drive is crucial when purchasing a used car from a dealership.

How can you negotiate the best deal at a used car dealership?

Negotiation is a normal part of buying a used car and one of the best ways to get the best deal. Before visiting the dealership, research prices for the make and model you’re interested in across multiple car dealerships and used car lots. Know the market value, the average mileage, and comparable vehicles; this gives you leverage when negotiating. Be ready to walk away if the dealer won’t meet your price — there are many used cars for sale and many used car dealerships will want your business.

During negotiation, focus on the total cost rather than the monthly payment, as dealerships sometimes structure deals to make monthly payments look attractive while adding fees or lengthening the loan. Negotiate the price of the car first, then discuss financing and trade-in values. Use your financing pre-approval from a bank or credit union as a bargaining chip to get lower interest rates and better terms.

Do used car dealerships offer warranties and extended warranties?

Dealerships often offer warranties and extended warranties on pre-owned vehicles. Some used car dealerships offer certified pre-owned programs that include a limited warranty, inspection, and roadside assistance. Extended warranties can be helpful to cover expensive repairs after the factory warranty expires, but they come with additional cost. Weigh the benefits of buying an extended warranty against the price of potential repairs for the specific make and model.

Ask the dealer to explain what is covered, what is excluded, and whether the warranty is backed by the dealership or a third party. Check whether routine maintenance is required to keep the warranty valid. If a dealer pushes an extended warranty, don’t hesitate to ask the dealer for written terms and compare with aftermarket warranty providers to get the best deal.

What paperwork and steps are involved in the buying process at a dealership?

Understanding the paperwork and steps involved will make your shopping experience smoother. When you buy a used car from a dealership, expect to complete a sales contract, financing paperwork if applicable, and title transfer or registration forms. Dealerships may handle registration and temporary tags; ask what fees they will add to the cost of the car and request a written breakdown. Knowing the total cost of the car, including dealer fees and taxes, helps you avoid surprises.

Before signing, read all documents carefully and confirm that the figures match the negotiated price. Make sure any verbal promises — like repairs or included items — are written into the contract. If you’re trading in a car, review the trade-in appraisal and how it’s applied to your purchase. Don’t sign until you understand every line — this is a crucial part of purchasing a used car and ensures you know what to expect when shopping at a used car dealership.

How can you get pre-approved and compare interest rates?

Getting pre-approved by your bank or a credit union before visiting used car dealerships gives you negotiating power and clarity on how much you can pay. Pre-approval shows the dealer you’re a serious buyer and can help you compare the dealership’s financing offerings. Dealership financing may be convenient, but the interest rates can vary; use your pre-approval to secure better terms when possible.

Compare interest rates across multiple lenders and consider the total cost of the loan, not just the monthly payment. A longer-term loan may lower monthly payments but increase interest paid over time. Discuss both the interest rate and loan term with the dealer and don’t hesitate to ask for a written loan estimate to compare financing options accurately.

What should you expect when trading in or selling your old car at a dealership?

If you plan to trade in your old car, dealerships often make the process convenient by appraising and applying the trade-in value toward your purchase. Get multiple appraisals from different dealerships and online buyers to ensure you get the best deal. Research the value of your trade-in based on its make and model, mileage, condition, and vehicle history so you can negotiate confidently.

When the dealership appraises your car, they will inspect the vehicle and consider market demand for that kind of car. Be honest about issues and present maintenance records to increase value. Decide in advance how much you need to net from the trade-in to make the new purchase affordable; sometimes selling privately yields a higher price than trading in, so weigh both options carefully.

How do you choose the right make and model when shopping at a used car dealership?

Choosing the right make and model starts with identifying your needs: passenger capacity, fuel economy, reliability, and budget. Research the reliability and cost of ownership for specific models, and consider how mileage and vehicle history affect future maintenance costs. Many used car dealerships stock a variety of pre-owned makes and models, so narrow your search by your must-have features and safety ratings.

Test drive several similar vehicles to compare how each make and model handles and fits your lifestyle. Read reviews, check recall history, and confirm parts availability and service costs. Being clear about the kind of car you need will help the dealer help you find the perfect car and make the shopping experience more efficient.

What are the benefits of buying used cars from a dealership versus private sale?

Buying a used car from a dealership offers several benefits compared to private sales. Dealerships often provide a wider selection of vehicles, certified pre-owned options, and professional inspections. They also handle paperwork like title transfer and registration, and may offer limited warranties, financing, or extended warranties. These conveniences can make the total cost and buying process smoother for many buyers.

However, dealerships may add fees or have higher sticker prices than private sellers. Balance the advantages — such as test drive options, the ability to negotiate, vehicle history reports, and post-sale support — against price. If you value peace of mind and structured financing, a used car from a dealership can be a rewarding and sensible choice. Don’t hesitate to ask the dealer for details about used car dealerships offer and any dealership-specific programs.

Summary: Key takeaways when visiting a used car dealership

- Inspect the car thoroughly and request a vehicle history report to understand the vehicle history.

- Get pre-approved financing and compare dealership financing options, interest rates, and monthly payment scenarios.

- Take a thorough test drive and have a mechanic inspect the car when possible.

- Negotiate the price first, then discuss financing and trade-ins to get the best deal.

- Understand warranty terms and whether extended warranties are worth the extra cost for your used vehicle.

- Read all paperwork carefully and get dealer promises in writing before signing.

Finding a used car that suits your needs requires preparation, patience, and knowledge of what to expect when shopping for used cars. By inspecting, test driving, reviewing the vehicle history report, and comparing financing options, you can buy a used car with confidence. If you’re looking for a reliable used car from a dealership, Integrity Autoplex, a Used Car Dealer in Elkhart, IN, can help you find the perfect pre-owned vehicle. With careful research and clear negotiation, the benefits of buying used cars — lower depreciation, more choices, and often lower costs — make purchasing from a used car dealership a smart move when you want to buy a car that fits your budget and lifestyle.

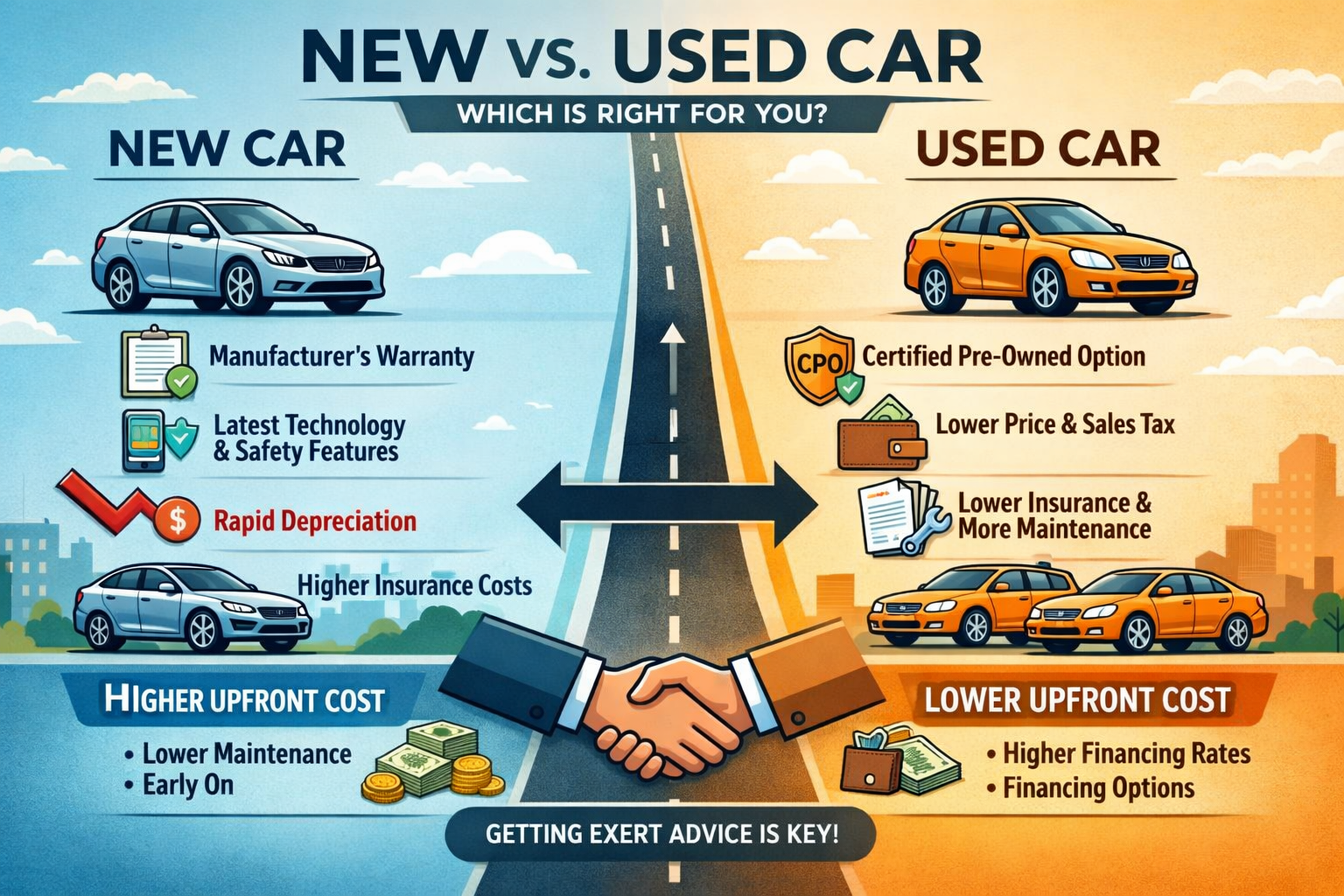

Difference between Used Car vs New or Used Car: What’s Better to Buy?

The difference between used cars vs new cars matters for every buyer deciding whether to buy a new or used vehicle. Choosing between a brand-new car and a used car affects price, depreciation, car insurance, warranty coverage, financing, and long-term cost of car ownership. This guide breaks down the important factors to help you decide whether buying used or buying new is right for your needs.

1) Is a used car or a new car better for my budget?

When deciding new or used car based on budget, the most obvious difference is price. New cars come with a higher sticker price and are typically more expensive than used cars, while a used vehicle may cost significantly less upfront. If you’re wondering whether to buy a new or used, consider that used cars often offer the greatest advantage of buying a used: lower purchase price and reduced sales tax in many areas.

Financing a new car usually means higher monthly car loan payments, whereas financing a used car may allow a smaller loan or shorter term. However, used car loans can have higher interest rates depending on credit and lender. Check both car loan offers and factor in car insurance—the new car may increase your premiums due to its higher replacement cost, while a used car might save you money on insurance.

2) What are the pros and cons of buying a used car from a dealer?

Buy a used car from a dealer offers benefits like certified pre-owned programs, dealer inspections, and often limited warranties. Buying used from a dealer can reduce risk compared with private-party sales because reputable dealers perform inspections and provide documentation. The pros of buying a used car include lower cost, slower depreciation, and potential for on-site service and financing options.

Cons of buying a used can include limited selection compared to new car inventory and potential for higher interest rates on used vehicle financing. When shopping for a car from a dealer, ask about vehicle history reports, warranties, and whether the dealer offers a buyback or return policy. Tips for buying a used include checking maintenance records and getting an independent inspection to avoid surprises.

3) How do depreciation and resale value compare between new and used cars?

Depreciation is one of the biggest differences between a new car and a used car. New cars lose value rapidly in the first few years—new cars often experience the steepest depreciation, meaning a brand-new car can lose a large percentage of its value as soon as it’s driven off the lot. That’s why many buyers choose a used vehicle: a used car has already taken the biggest depreciation hit, so its resale value declines more slowly.

If you plan to sell or trade the car in a few years, a new car may cost more in terms of depreciation. Buying used can preserve more of your investment because the car is worth less upfront but may hold value more consistently over time. Weigh the pros and cons of buying used vs buying a new car by estimating depreciation for the specific make and model you want.

4) Are warranties and reliability better with a new car or buying used?

One advantage of buying a new car is the manufacturer warranty and the peace of mind that comes with a brand-new vehicle. New cars come with warranties that cover many repairs for the first several years, and new car buyers often enjoy roadside assistance and promotional maintenance plans. These benefits reduce unexpected repair costs early in ownership.

However, buying used from a dealer doesn’t necessarily mean you lose warranty protection. Certified pre-owned programs and dealer-backed limited warranties can offer coverage for certain repairs. When buying used, check whether the used car has remaining factory warranty, if there’s a certified program, and whether extended warranty options are available to offset concerns about potential repairs.

5) How do car insurance costs differ for new vs used vehicles?

Car insurance often costs more for a new car because insurers base premiums on replacement cost, repair cost, and likelihood of theft. A new vehicle may be more expensive to insure due to higher replacement value and cost of new parts. If you’re deciding whether to buy a new or used, factor insurance quotes into your monthly budget to avoid surprises.

Used cars usually have lower insurance premiums, especially if you choose to drop certain coverages like gap insurance. However, an older car might lack modern safety features that can lower premiums, so get insurance quotes for both the new vehicle and the used one you’re considering. This comparison should be a key part of your car buying research.

6) Should I buy new for the latest features or buy a used vehicle to save money?

New cars come with the latest technology, safety features, and fuel-efficiency improvements. If you want the newest driver-assist tech, infotainment systems, or better fuel economy, buying new makes sense. The advantage of buying a new vehicle is access to the most up-to-date features and manufacturer updates.

Buying used can still get you many of the modern features at a lower cost—cars that are only a few years old often include advanced safety systems and smartphone compatibility. Consider whether you need the newest features or whether a slightly older model meets your needs. Often the best balance is a used car that’s a few years new enough to include important safety and convenience features while being significantly cheaper than a brand-new car.

7) How does financing a new car compare to a used car loan?

Financing a new car often comes with promotional rates or incentives from manufacturers—buyers may find lower APR financing for new vehicles. Financing a new car may be easier to qualify for at favorable rates, making the decision to buy new attractive for those with strong credit. However, the total loan amount tends to be larger because new cars are more expensive.

Financing a used car typically means lower loan amounts and possibly shorter loan terms to avoid being upside-down (owing more than the car is worth). On the other hand, used car loans sometimes carry higher interest rates. When deciding whether to buy new or used, compare monthly payments, interest rates, and total cost of financing to see which option better fits your financial plan.

8) What are the pros and cons of buying a certified pre-owned used car?

Certified pre-owned (CPO) vehicles can offer the benefits of a used car with added warranty protection and dealer inspection. Pros of buying a CPO include extended warranties, multipoint inspections, and often special financing options. This makes a certified used car an appealing middle ground between brand-new and older used vehicles.

Cons of buying CPO can include higher prices than non-certified used cars and limited selection. Evaluate the CPO program carefully: check what the warranty covers, the length of coverage, and whether the vehicle has passed a rigorous inspection. For many buyers, a CPO vehicle balances the advantages of buying a new car (reliability and coverage) with the savings of buying used.

9) How do maintenance and repair costs compare between new and used cars?

New cars may have lower maintenance and repair costs in the first few years because they’re under warranty and parts are new. Routine maintenance like oil changes and tires still apply, but major repairs are less likely when you buy a new car. This can make overall cost of car ownership lower initially for a new vehicle.

Used cars might require more maintenance depending on age, mileage, and previous care. However, many used cars are reliable and affordable to maintain, especially if they’re well-maintained models with good reliability ratings. Pros and cons of buying used include potential for more frequent repairs but lower initial cost; weigh anticipated maintenance against savings on purchase price.

10) How do I decide whether to buy new or used—what factors should I weigh?

Deciding whether to buy new or used comes down to key factors: budget, how long you’ll keep the car, desired features, financing and insurance costs, and tolerance for depreciation and repairs. If you want the newest features, worry-free ownership, and warranty coverage, buying new may be better. If you want lower upfront cost, slower depreciation, and more value per dollar, buying used is often the smarter choice.

To decide, make a checklist: price range, target monthly payment, must-have features, acceptable mileage, and whether you prefer dealer-backed warranties. Shop both new and used options, get quotes for car insurance and financing, and test drive candidate vehicles. That process will help you weigh the pros and cons and choose the right type of car for your situation.

11) What practical tips should I follow when buying used to avoid common pitfalls?

When buying used, follow practical tips to reduce risk: obtain a vehicle history report, have an independent mechanic inspect the used car, verify title and maintenance records, and take a thorough test drive. These steps protect you from hidden issues and ensure the used one meets your expectations. Also, negotiate price—used vehicles typically have more room for negotiation than new cars.

Other helpful actions include checking recall status, confirming the car’s VIN matches paperwork, and comparing prices across dealerships and private sellers. If you plan to finance, shop around for the best car loan rates and consider a shorter loan term to avoid paying more interest over time. These measures will improve your chances of buying a dependable used car with fewer surprises.

12) How do environmental and long-term value considerations differ between new and used vehicles?

New cars often include better fuel economy and lower emissions thanks to advances in technology—new cars may be more environmentally friendly per mile. If environmental impact is a priority, buying a new vehicle with improved fuel efficiency or opting for hybrid or electric options might be preferable.

Conversely, extending the life of an existing used car can be environmentally responsible because it reduces resource consumption associated with manufacturing new cars. The difference between a new and used car in environmental terms depends on the age, efficiency, and lifecycle considerations of the vehicle. Consider total cost of ownership and environmental impact together when deciding whether to buy new or used.

13) Can I get better value by buying a slightly used car that’s a few years old?

Buying a car that’s a few years old often provides excellent value: you avoid the initial depreciation hit that new cars suffer while still getting relatively modern features and reasonable reliability. Cars that are a few years old combine many advantages of buying new (safety features, recent technology) with the cost savings of buying used.

Look for well-known reliable models and consider certified pre-owned options if you want additional warranty coverage. Financing a slightly used car can also be favorable because loan amounts are lower yet the vehicle still feels modern. For many buyers, this middle ground—buy new or used?—leans toward buying a used one that’s recent enough to meet expectations without the new car premium.

14) What are the pros and cons of buying from a dealer versus a private seller?

Buying from a dealer, especially an established one, offers the advantages of consumer protections, potential warranties, and often financing options. Dealers can help buyers navigate car insurance and car loan paperwork, and dealers often provide servicing. Pros of buying from a dealer include legal protections and easier trade-in or sale down the road.

Private-party sales can offer lower prices but come with fewer protections. If you buy from a private seller, you must be diligent about inspections, title transfers, and ensuring the car is worth the price. Whether to buy from a dealer depends on your comfort with risk and your preference for convenience, warranty coverage, and financing help.

15) How should I compare total cost of ownership for new vs used?

Total cost of ownership includes purchase price, depreciation, financing costs, insurance, taxes, maintenance, repairs, fuel, and potential resale value. To compare new vs used, create a spreadsheet estimating each category for the specific models you’re considering. This objective approach reveals whether buying used or buying new better aligns with your finances and lifestyle.

Don’t forget to include intangible factors like peace of mind, warranty coverage, and how long you plan to keep the car. A new car may reduce uncertainty in the short term, while a used car may deliver better long-term value due to slower depreciation and a lower initial investment.

16) Where can I find reliable used cars and what should I expect from dealerships?

Reliable used cars are available at certified pre-owned programs, independent used car dealers, and reputable franchised dealerships. When shopping, expect transparency about vehicle history, inspection reports, and warranty options if you buy from a dealer. Ask for a test drive, maintenance records, and third-party inspection to ensure the used car meets your standards.

Dealerships may offer trade-in assistance and financing that simplifies the process of buying a used car. If you prefer a faster, lower-risk transaction, buy a used car from a dealer rather than a private seller. Evaluate dealer reviews and reputation to make sure you’re getting trustworthy service and a reliable used vehicle.

17) What are final tips to decide new cars vs used cars for different buyer types?

If you value the latest safety tech, warranty coverage, and low maintenance in the first years, a new car is often the right choice. Buyers who drive long distances, need the best fuel economy, or want the newest features may prefer a new vehicle. If you’re budget-conscious, want lower monthly payments, and prioritize value, buying used or a certified pre-owned model is usually smarter.

For first-time buyers or those on a tight budget, a reliable used car can provide mobility at a manageable cost. For buyers focused on long-term ownership and fewer maintenance concerns, a new car may be attractive. Ultimately, weigh pros and cons, get multiple quotes for car insurance and loans, and test drive several options before deciding.

Summary: Key takeaways on the difference between used cars vs new cars

- Cost: New cars are more expensive initially; used cars typically cost less upfront and depreciate slower.

- Depreciation: New cars lose value fastest in the first years; used cars have already taken that hit.

- Warranties & reliability: New cars come with manufacturer warranties; certified used can offer some protections.

- Insurance & financing: New cars often mean higher insurance and larger car loans; used cars may have higher loan rates but lower premiums.

- Features & environment: New cars come with the latest tech and efficiency; used cars can still offer modern features at lower cost.

- Dealer vs private sales: Dealers offer protections and financing; private sales may be cheaper but riskier.

- Total cost of ownership: Consider purchase price, depreciation, insurance, maintenance, and resale when choosing.

Choosing between used car vs new car depends on your budget, priorities, and how long you plan to keep the vehicle. If you’re ready to buy a used car from a dealer and want expert help finding a reliable used vehicle, consider Integrity Autoplex, a Used Car Dealer in Elkhart, IN. They can assist with trade-ins, financing a used car, and providing inspections so you can weigh the advantages of used car ownership and the pros and cons of buying used versus new. Whether you decide to buy new or used, use the tips above to find the right car for your needs and budget.